Every financial guru that I have ever run across starts out with teaching people how to do a monthly budget. It is absolutely the best way to start getting your finances in order.

The problem is that most people who are budgeting for the first time are living paycheck to paycheck, and budgeting for an entire month when you are just barely or not quite making it through the month is really difficult.

I frequently hear comments like, “How do I know which paycheck pays which bills?” And that is where the monthly budget falls short in helping people.

The solution is a monthly budget with a twist. Instead of looking at the entire month as a whole we want to break each week down and conquer them individually so that by the time we reach the end of the month we are winning with our budget.

Quick Navigation

Using a Monthly Budget Organized By Week

Since all of our bills come in each month, we still want to be able to look at the month as a whole. The problem is trying to jam all that information into one single column is really hard when you are living paycheck to paycheck.

That is why we turn to the “Weekly Budget” found on the budgeting tools page of the I Was Broke. Now I’m Not website.

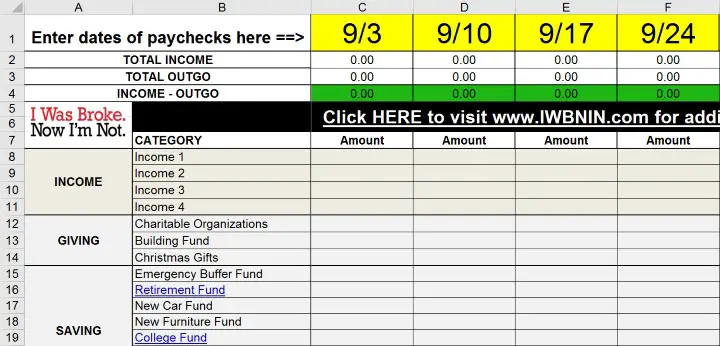

Once you download the weekly budget and open it in your favorite spreadsheet program it is going to look something like this:

At first glance this makes the eyes of people who do not like budgeting cloud over and they start to doze off from math avoidance.

DON’T AVOID THIS BUDGET FORM. Once you start using it, it will all make sense, and the form does all the math for you so no worries there.

Fill In Your Income

Since our income is the most fun part of any budget we start with that first. Whether you are receiving pay from one employer or multiple employers there are enough row to make sure you are able to fit them in.

You want to make sure you put in each paycheck on the corresponding week. In this example, I get paid every two weeks, while my wife gets paid bi-monthly.

This means that some months we will get paid on the same week while others we will have different pay days.

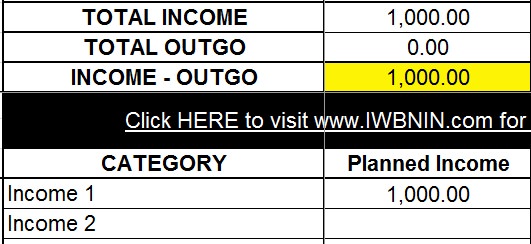

You are going to notice that the color of the total box in the scoreboard is going to change colors (Income-Outgo). Green means you are good.

You spent all the money for that week to exactly zero. Red means you have over spent that week and yellow is there to warn you that you have unspent money in your budget.

This may seem a bit over the top but the yellow is really important. When we leave money in our budget and do not give it a purpose it tends to magically disappear.

It’s like leaving the house with a 20 dollar bill in your pocket. Later that day you come home with $2.17 and have no idea where the money went. The same thing happens on a larger scale when you don’t tell you money where to go inside of your budget.

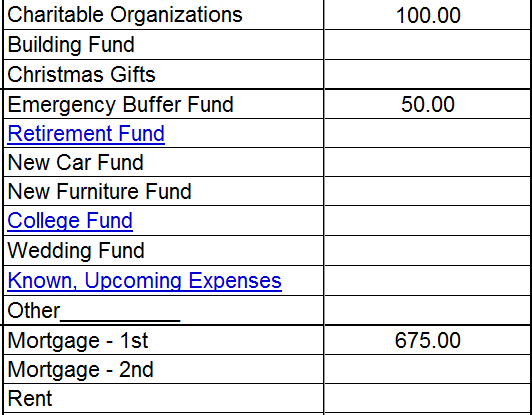

Plug in Your Expenses

This is where paycheck-to-paycheck budgeting gets more difficult than doing an entire month at one time. You will need to fill in each expense based on when it is due and match that up with the corresponding week.

That way you know which paycheck pays which bills.

At this point in the process we are just trying to get every expense into the budget that we have along with the correct due dates on all your bills. Don’t worry about doing any balancing until you are absolutely sure that you have everything in here.

If you are doing a budget for the first time and aren’t sure that you got everything, the budget form is editable so add a “WE FORGOT” category and throw a couple hundred dollars in there to make sure you know you got the forgotten stuff covered.

Remember to Save

Many people do a budget and then whatever is left over at the end of the month is put into savings. This is completely backwards.

We want to include our savings as a part of our overall spending. So there are rows on the budget form that allow you to “spend” your money into savings.

This is why I recommend having a separate savings account that you can move money out of your checking and put it out of sight, out of mind.

This way you won’t be tempted to “accidentally” spend that money that should be going into your savings account.

Balancing the Budget

Now go through and get your budget to where it balances to exactly zero for each week. This may mean cutting out some expenses that you really want to keep.

For some people this is an eye opening experience where you realize you are spending too much on restaurants or on entertainment.

You can move items around like savings or maybe reduce your grocery budget for one week and make up for that reduction the next week to make sure you are still getting the food your family needs.

Some Paycheck to Paycheck Budget Balancing Tips

So you got to the end of you budget and you are seeing red boxes across the top. You may feel like you have cut your budget to the bone, but you came to the website of the guy nicknamed the “Saving Freak”.

So here are some ways that I know people cut their budgets when they thought it was impossible:

- Cut Food Costs – Food makes up a major part of every family’s monthly expenses. You can cut dining out costs by looking for a deal, eating out less, or only going to places where kids eat free. Most people can cut their grocery budget by use coupons strategically or switching to Aldi for most of their shopping

- Get new insurance quotes – We often forget that insurance rates go up over time when you stay with the same company. Get a new set of quotes for your cars, home, and everything else to make sure you are paying the right amount.

- Adjust Your Withholding – I know a ton of people that like getting a big tax return. If you are one of these people, talk to HR and adjust your withholding so that you get more money into your monthly budget.

- Go to Cash Envelopes – If you see an area where you are overspending, switch that category over to cash. Take the money out each pay period for that category and put it into an envelope. When the money is gone you cannot spend any more. This way you stop the overspending cold.

Need Some Extra Help?

If you are still having problems getting your budget to work, I suggest trying some more detailed training. The resource I like the best is the I Was Broke. Now I’m Not. Group Study Participant Kit.

It only costs $30 and works as a self study in getting your finances in order. Just read the book and fill out the guide and you can get your budget in order.

If you like something more video oriented, the I Was Broke. Now I’m Not. Core Budgeting Program. This is an online coaching program with directed videos that allows you to get your budget in order and get help with each step.

It is part of a larger program that will be launching very soon. Just like the book it will only cost you $30.

Final Thoughts on Paycheck to Paycheck Budgeting

You need to have a budget. It is the engine that will drive your financial success. If you are not using a budget then you are not working at full capacity in your finances.

Even if you are just starting out while living the paycheck to paycheck lifestyle, Budgetting is what will help you get out of that stressful situation.

Nicole VanOrder says

Now that we’re past the holidays, a lot of people are focused on fitness. Personally, my husband and I are currently weighing the options of paying for a gym membership v. buying some home exercise equipment, so I was wondering if you could offer some tips about purchasing home exercise equipment. In the warmer weather, we garden, and take bike rides, walks and the like, but in the winter, it’s hard to get out to excercise.

Although this is the first time I have commented, I love the site, and enjoy reading the updates.

Keep up the good work! – Nicole